Ending the Innovation Theater Cycle — Why the Real AI Danger Isn’t What You Think.

Citrini’s AI Doomsday Won’t Happen. What Will Is Worse.

On February 22, 2026, Citrini Research published a scenario — deliberately labeled as such, not a prediction — that briefly moved markets and generated tens of millions of views. The scenario imagined a memo from June 2028 looking back at how AI had triggered a “Global Intelligence Crisis”: AI agents replace white-collar workers at scale, corporations reinvest the savings into more AI, displaced workers stop spending, the consumer economy contracts, and the S&P falls 38% from its highs. Michael Burry amplified it on X. The Dow dropped over 800 points as software, payments, and financial stocks sold off. Bloomberg called it a “doomsday narrative” that had “taken Wall Street by storm.”

The backlash was swift. Citadel Securities, Deutsche Bank, Fidelity International, and a White House economist who called it “science fiction” all pushed back. Both sides are now arguing about whether AI will replace Western workers fast enough to trigger a demand collapse.

Makes perfect sense. But I would say, it´s the wrong debate.

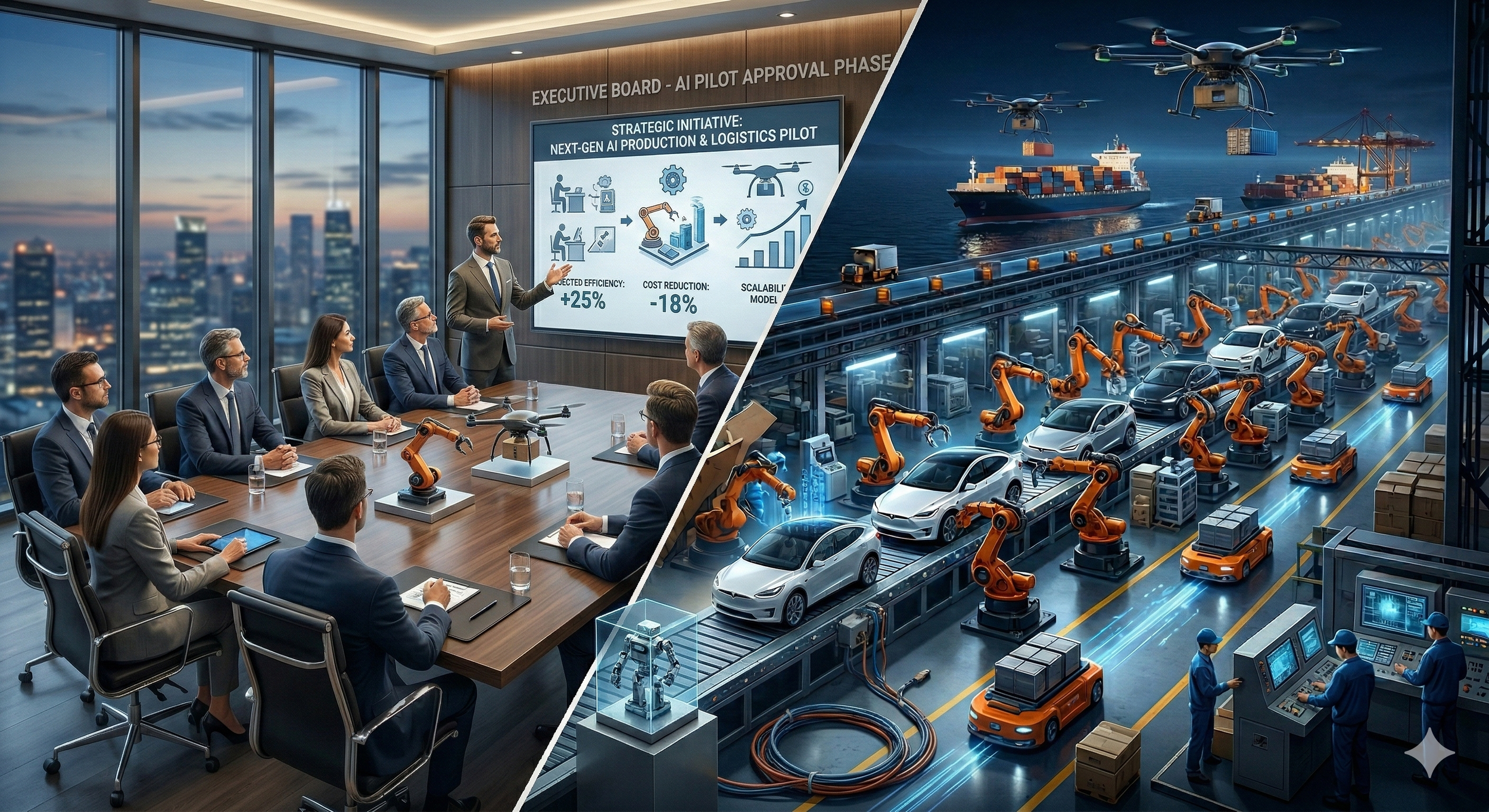

The Citrini scenario requires Western companies to actually deploy AI at scale — rapidly and deeply enough to displace significant white-collar employment within two years. But how much progress have Western enterprises made capitalizing on AI over the last two years? And isn’t this just the latest chapter in twenty-five years of digital transformation initiatives that never made it past the pilot stage? Western companies are good at optimizing what they already have. But AI and the Citrini text promise something bigger — that is where the track record falls apart. And it says something that the current AI conversation is dominated by LLMs — the one form of AI that is best at generating demos, not revenue.

Meanwhile, Chinese competitors are already deploying AI across manufacturing, logistics, and customer service — not as pilots but as production infrastructure. The real danger is not that AI will replace Western workers. It is that competitors who are actually building with AI will replace Western companies — while those companies are still running their third pilot.

It comes down to this: US tech companies build narratives for investors. Their goal is to grow market cap. Chinese companies build products for people. Their goal is to earn money with customers. Western enterprises, caught in the middle, keep buying the narratives — and rarely ship something scalable.

For a long time, this Western approach worked great. Everybody got rich. But I am afraid that era is ending. Let me explain why. And sorry if it takes a bit longer than my usual texts. But it is worth the time. I promise…

(Btw, before we start let me state the obvious: of course, there are always exceptions — US companies that build real products and Chinese companies that waste time on theater. But the structural patterns are clear enough — and consequential enough — that sharpening the contrast is more useful than hedging it.)

Digital Transformation — Twenty-Five Years of Digital Stagnation.

The defining business narrative of the past quarter century has been Digital Transformation. It promised to modernize every industry, every function, every process. It produced an enormous amount of activity. What it did not produce, in the vast majority of cases, was actual change. McKinsey and BCG estimated that roughly 70 percent of digital transformations failed to meet their stated objectives.

To be fair: Western companies are often quite good at using technology to optimize what already exists — making established processes more efficient, reducing costs, improving margins. But that is not what Digital Transformation promised. It promised fundamental change. New products, new business models, new ways of creating value for customers. And that is what it rarely delivered.

At the same time, Digital Transformation was never one thing. It was a container, cycling through whatever technology narrative was current. Open an innovation lab, adopt agile, partner with startups. Each wave — Big Data, Blockchain, Web3 — carried its own hype, its own vendors, its own conference circuit.

The pattern was always the same: lots of investment. Real professionalism. But no lasting change. Instead it usually produced what it was actually optimized to produce: not a better product for customers, but a better narrative for investors. Digital Transformation, as practiced, is often not a strategy for change — it is a strategy for the appearance of change. And it worked, because no competitor was doing anything different.

The Solow Paradox — Proof This Is Not New.

The pattern predates even the trends described above. In 1987, the Nobel laureate economist Robert Solow observed: “You can see the computer age everywhere except in the productivity statistics.” Companies were investing in IT and hiring technology consultants at an accelerating rate. And yet, measured productivity growth was not rising as one would expect. This became known as the original Solow Paradox — and it was kind of resolved, but only a decade later, when companies actually restructured their operations around the technology rather than bolting it onto existing processes.

The Solow Paradox was not a failure of technology. It was a failure of organizational adoption. The technology worked. The organizations were not willing or able to change how they operated in order to use it. And this problem is still with us today.

In 2018, McKinsey published a report titled “Is the Solow Paradox Back?” — arguing that despite the explosion of cloud, mobile, and early AI, digitization was once again everywhere except in the productivity statistics. The diagnosis was the same as Solow’s, three decades later: the technology is available, but the organizations are not changing.

In 2025, McKinsey identified what it calls the “GenAI Paradox”. Nearly eight in ten companies report using generative AI — yet roughly the same proportion report no significant bottom-line impact. The copilots and chatbots that have been scaled deliver diffuse, hard-to-measure gains — combined with lots of AI workslop. The vertical applications that could actually transform operations rarely make it past the proof-of-concept phase. And it doesn’t help that the Western AI conversation is almost entirely focused on Large Language Models (LLMs) — the most visible and most demo-friendly form of AI, but far from the most useful for many business applications. Machine Learning, predictive analytics, optimization algorithms — these are often where AI creates real operational value. But they don’t make for good keynotes.

1987. 2018. 2025. The same paradox, keeps coming back every few years, diagnosed with fresh terminology. Maybe because nobody has looked closely enough at the process that keeps producing it?

The Innovation Theater Cycle.

The examples above are not random failures. They follow a recognizable pattern, which emerges around nearly every innovative technological shift in the West, with remarkable consistency.

Stage 1: The Hype Machine Starts. A new technology appears. It is real — in many cases, early adopters somewhere in the world are already deploying it at scale. But in Western boardrooms, it is still a concept. Vendors, analysts, and consulting firms recognize the commercial opportunity immediately. Whitepapers, conferences, practice areas — the commercial infrastructure builds overnight. The Gartner Hype Cycle becomes a self-fulfilling instrument, which simultaneously describes the hype and contributes to it. FOMO sets in among executives. Budget conversations begin.

Stage 2: Vendors Sell the Vision, Companies Buy Proofs of Concept. Consulting firms and software vendors offer to “explore the opportunity together” — at the client’s expense. Proofs of Concept are scoped to succeed: controlled environments, cherry-picked use cases, vendor engineers on-site. Vendors collect fees and, critically, case studies they can use to sell the next client. Everyone declares the pilot a success.

Stage 3: Scaling Reveals the Real Problem. Moving from a controlled pilot to production-grade deployment exposes everything the PoC was designed to avoid: decades of legacy infrastructure, organizational silos, disputed data ownership, and the political reality that real transformation threatens real people with real power. Vendors propose additional engagements to “solve the complexity.” Costs grow. Timelines extend. Results do not materialize at the promised scale.

Stage 4: Declare Victory and Move On. Everyone starts to lose interest. The initiative is quietly scaled back or rebranded. The original PoC is featured in the annual report as evidence of digital leadership. No one is held accountable because the vendor can reasonably blame organizational resistance, and the organization can reasonably blame the technology’s limitations. Both narratives contain partial truths, which makes them hard to challenge. Then the next trend appears and consulting firms rebrand their practice areas. And because no competitive pressure materialized and everyone was happy, there is no urgency to approach the next wave differently.

Four stages. And endless loop. Expensive, but professionally managed, and almost always without much change or lasting economic value created. In a way, the Innovation Theater Cycle is the engine that keeps the Solow Paradox running. Yet nobody seems to see a problem in that.

Why Nobody Cares.

Why does the cycle persist? Not because people are stupid. But because it makes sense for everyone involved:

No real competition. Today, many Western incumbents face no serious challenge — especially in tech: new ideas from startups like WhatsApp or Instagram get crushed or bought. Innovation is about signaling, not survival.

The target group is investors, not customers. This is the heart of it. Especially for the tech giants, where the often monopolistic core business hums along and brings in huge profits, building radically new products at scale is risky. It could fail. Same is true for many non-tech enterprises. A PoC, on the other hand, is a near-perfect capital markets instrument: tangible enough to announce, contained enough to succeed, cheap enough that the narrative ROI is positive — even if it produces nothing. The product is the narrative. The customer is the investor. Same is true for the backend: real transformation takes years, cannibalizes existing revenue, and creates the short-term earnings impact that institutional investors punish.

PoCs are also great for vendors. They keep expectations low and ensure the deliverables are indeed deliverable. Even if it fails at least everyone learns. A constant stream of ambitious-sounding Proofs of Concept with great PR fanfare generates reliable recurring revenue — and new leads. This is not a conspiracy. It is an incentive structure.

The cycle works for executives, vendors, analysts, and capital markets. The only constituency it does not work for is customers — but customers, in this model, are not the primary target group.

This arrangement had one critical dependency, though: that competitors approach innovation with the same mindset. If everyone is mostly fine with doing Innovation Theater, no one falls behind. A remarkably stable system — as long as it remains closed.

And this is no longer the case.

The big US tech monopolies look like they are always very innovative. But at the core, they follow the growth narrative approach the hardest, without really changing products & services: Apple releases the same iPhone every year with a different number. Google and Meta still rely on the same one-trick pony business model. When something radically new comes along like AI, they quickly use their monopoly profits to make sure they don’t fall behind. But always focusing on building growth narratives. The customer-facing core UX doesn’t change all that much.

The one exception? Instagram. And why did Instagram change? Because it was forced to by someone that couldn’t be crushed or bought: TikTok, coming from China. Suddenly there was competition.

How China Is Different.

Chinese technology companies never got lost in the Innovation Theater Cycle, because the competitive environment made it unaffordable for them.

The Chinese domestic technology market is one of the most brutally competitive environments in the world. Margins are thinner, imitation faster, and the number of well-funded competitors larger than in almost any equivalent Western market. A company that spends eighteen months running a Proof of Concept while a competitor scales the same technology into production does not get to declare victory in the annual report. It just ceases to exist.

The consequence is a fundamentally different relationship with innovation. In Chinese tech companies, the Proof of Concept and the production deployment are often the same conversation. The question is not “does this technology work in principle” but “how quickly can we get this into revenue-generating operations.” Failure is expected — not as a reason to retreat to a press release, but as operational data to be incorporated in the next iteration.

The data infrastructure, the engineering culture, the organizational agility and readiness to really change products — these were not just strategic initiatives. They were and still are much needed survival requirements. In this world, revenue is the KPI. The product is the means to achieve it. And the target group is still the actual customer.

Chinese Competitors Suddenly Compete. Here.

Chinese tech giants like Alibaba and Tencent were always reluctant to bring their flagship products — like TMall or WeChat — cross-border. The domestic market was so full of potential that it was not necessary. But that has changed.

China’s domestic economy is under significant structural pressure — property market stress, slower consumer growth, a cautious middle class. At the same time, TikTok, SHEIN, and TEMU have proven that every Chinese enterprise not going cross-border is leaving money on the table. Internationalization has shifted from an interesting option to a strategic necessity.

So, SHEIN and TEMU were just the start. And while this first wave was about price, the next will be about value.

Xiaomi already proved this with smartphones that match flagship specs at a fraction of the price. In 2027 it is planning on bringing the same approach to European electric vehicle markets: a beautifully designed, tech-integrated car that Western automakers cannot build at that price point.

Pop Mart turned creative collectible toys into a global brand with a fiercely loyal fanbase — a product-led success story that no Western competitor saw coming.

Anta Sports has overtaken Nike in Chinese market share, not by being cheaper but by being better at product innovation and digital integration — and in January 2026 announced its plan to acquire a 29% stake in Puma, buying its way into the European market with €1.5 billion in cash from internal reserves.

These companies arrive with scale, capital, manufacturing depth, and operational excellence, hardened by the fight for more customers, not loftier narratives. And they are all right now figuring out what to do with AI across the whole value chain. They are not waiting for AGI to tell them.

AI in China: Revenue, Not Theater.

Western companies talk about being AI First a lot. But most still don’t really know what it means — hence the GenAI Paradox: 78 percent adoption, 80 percent reporting no material bottom-line impact. The same structural failure wearing its third name in four decades.

OpenAI is a case in point. In September 2025, they announced with great fanfare — partnerships with Shopify, Etsy, Stripe. Millions of products coming to ChatGPT. The future of AI commerce. In March 2026, that future is already the past, the project was quietly scaled back. The idea of true Agentic Commerce was just another narrative.

Now compare that with what Alibaba Group has been building in the same time: Their Qwen Agent — One-Sentence-Shopping — lets you say what you need and it handles everything: searches across platforms, orchestrates logistics, completes payment via Alipay. True Agentic Commerce already at scale: 100 million users. 400+ tasks. And 10 million orders of bubble tea in 9 hours during a campaign on Chinese New Year 3 weeks ago.

Same use case. One built for a press release. The other built for customers.

And Qwen Agent is not the only example for AI deployment operating at scale in China:

SHEIN is a true AI-first company, although almost nobody sees them as such. But they understood AI not as a tool but as a platform — and built the biggest fashion retailer in the world on it.

Alibaba’s chatbot Accio does not just generate images of imagined products — it generates entire supply chains for them.

And then there are dark factories driven by AI — like the one from Xiaomi: so highly automated that the lights can be switched off. Not a Proof of Concept. They produce 40 cars per hour. For over a year.

Chinese companies are not playing a different version of the same game. They are playing a different game entirely. The difference isn’t just execution. It is ambition: Western companies use AI to save money. Chinese companies use AI to grow.

Back to Citrini — The Real Danger.

Which brings us back to where we started.

The Citrini scenario requires Western companies to deploy AI at scale, rapidly and deeply enough to displace significant white-collar employment within two years. How likely is this considering the track record of the last twenty-five years?

It might happen. But isn’t it more likely that we will run into the usual hurdles? Sure, the CDO will present a good-looking AI strategy and pretty convincing PoCs will be built. But once we try to scale them, we realize that data is still not available across the various silos and company politics once again stalls the rollout.

The organizational inertia, the legacy infrastructure, the capital markets orientation, the vendor dependency — all of the forces we just described above will slow AI deployment just as they slowed every previous trend. In that case the Innovation Theater Cycle could paradoxically be an effective buffer against the Citrini scenario.

But that doesn’t mean we’re safe. The Citrini nightmare could still come true — just not the way the doomsayers think.

Because here is the real danger scenario:

While Western companies safely run through the Innovation Theater Cycle on AI, Chinese competitors do the actual deployment. They build AI into their products and operations. They drive down cost structures. They improve what customers actually get. And then they arrive in Western markets with capabilities that Western incumbents simply cannot match.

The displacement that follows is not of workers by AI. It is of entire Western industries by Chinese competitors who built products while the West was building narratives.

It is slower than Citrini’s crash, quieter, harder to see coming, and harder to reverse once it has arrived. And unlike Citrini’s scenario, it does not require anything to go wrong. It only requires things to continue exactly as they have been.

It’s Time to Break Out of the Cycle.

No matter which scenario comes to pass in the end, the lesson is the same: it is time to stop rehearsing and start building.

If “this time it is different” is true, it is not because a Super Intelligence is about to arrive — even if it does one day. It is because the changes AI drives are falling together with large geopolitical shifts. The West has been predicting the rise of Asia for decades, but it was always something that was supposed to happen in the distant future — so we missed that it already happened.

The combination of what AI makes possible and the changes in the global competitive landscape means this time things really are different. The Innovation Theater Cycle needs to break — not because a consultant says so, but because the competitors arriving in your market have never heard of it.

A good first step is to stop looking only to Silicon Valley and start studying what is happening between Chengdu and Shanghai. The answers are not in the next whitepaper. They are in the products that are already being built — for actual customers, generating actual revenue, at a scale that should keep Western boardrooms up at night.

And perhaps the reason we are still so blind to what is happening in China is that the Innovation Theater Cycle has shaped our expectations towards innovation in general. After twenty-five years of PoCs that seldom scale, we find it normal not to expect real results — from ourselves but also from anyone else. When a Chinese competitor shows up with a product that actually works at scale, the instinct is to dismiss it rather than understand it. The cycle doesn’t just prevent us from building. It prevents us from wanting to learn.

But getting new ideas from studying places that do things differently could also mean an opportunity, especially for Europe.

While US tech burns through hundreds of billions chasing AGI, European companies could take a page from the Chinese playbook: skip the narrative, focus on operational AI that actually improves products and processes — and do it with open-source models that don’t require Silicon Valley-sized budgets. The tools are available. The question is whether European companies will use them to build, or use them to run another PoC…!?